Single-Family Rental Had Its Day. What Comes Next?

Parallels between SFR in the aftermath of the Global Financial Crisis and small multifamily post-COVID

The Global Financial Crisis fundamentally changed the course of the real estate industry in the United States in many ways. One often overlooked effect was its role in the creation of an institutional SFR (Single-Family Rental) industry by bringing a supply of millions of suburban single-family homes onto the market, often in highly discounted distressed sales or foreclosures. The current financial crisis, the CFC (COVID Financial Crisis) has different root causes, different government policy interventions, and unique ongoing impacts. However, like the prior crisis, the CFC is shifting the real estate market in fundamental ways and is priming the institutionalization of another asset class, in this case by foreshadowing a rollup of small (2-20 unit) multifamily urban properties, a multi-trillion-dollar asset class currently mostly owned by small operators.

This essay will explore how policy interventions implemented during the CFC are 1) propping up single-family home prices, 2) putting unique stresses on operators of small multifamily assets, and 3) creating a dramatic gap in cap rates between the single-family, small multifamily, and large multifamily asset classes.

Housing creation never recovered from the GFC

The subprime mortgage crisis triggered a cascade of events that destabilized the financial system, cratered home values nationwide, and resulted in a period of underinvestment in housing that arguably has yet to end.

In addition to the drop in new housing development, the Federal Reserve Board of Chicago estimates that there were roughly 3.8 million foreclosures on single-family homes between 2007 and 2010. This is roughly the same number of homes that were started between 2009 and 2014. More recently, just 1.5 million new home starts were recorded in 2022, still well below the peak of 2 million homes in 2005.

A glut of distressed single-family homes created the SFR market

In the midst of this turmoil, a number of investors and entrepreneurs spotted an opportunity. Part of the collapse in single-family home prices was caused by genuine oversupply that demanded a price correction, but another part was an overcorrection driven by financial contagion that resulted in bulk fire sales of these homes at a fraction of their true value. Tightening credit left many owners holding mortgages on homes they couldn’t afford to keep.

Operators like Invitation Homes recognized that these conditions were likely temporary and began purchasing single-family homes en masse on the (correct) assumption that their value would quickly recover. The undervaluation of these assets created slack that allowed operators to develop new technology, management processes, and acquisitions strategies that soon scaled up to serve as the best practices playbook for the new single-family rental (SFR) industry.

Government intervention disrupts normal market processes

Over the past decade, the SFR space has matured, with more competition between operators, a higher degree of capitalization, and more public visibility. These secular trends make it harder to acquire efficiently across the asset class, and are unlikely to durably reverse. On top of this, in the wake of the COVID pandemic, government intervention created a flood of cheap debt (spurring institutional and individual buyers) and effectively banned foreclosures, protecting those impacted by COVID job losses from losing their homes. This, along with other forms of financial support, drove housing prices to new heights.

The momentary institutional buying spree enabled by the pandemic, increasingly expensive debt, pent up demand from would-be homeowners, and sellers holding out for higher sale prices are pushing single-family home prices out of reach for corporate landlords. Once the biggest buyer of SFR inventory, Invitation Homes has gone from buying $150M worth of houses per week to buying only 470 houses in the first half of 2023, while selling 675 in the same period. Despite popular narratives, SFR operators are often net sellers of housing these days. In many cases, asset appreciation has driven SFR yields below those of treasuries, prompting would-be institutional buyers to hold off until better opportunities arise or to direct their capital elsewhere.

Lower rates won’t change the equation—SFR is never coming back.

On top of this, the anticipated reduction of interest rates at some point in 2024 is unlikely to lead to the reopening of the SFR market for institutional buyers. Under the current high rate environment, both buyers and sellers are rationally refraining from transacting, resulting in a 13-year low for home sales and massive backlog of home demand. This is on the back of a decade of underproduction in housing overall. When rates do drop, individual buyers, many of whom are millennials eager to progress in their homeownership journey, will re-enter the market, bidding up prices even further out of reach for returns-conscious institutional acquisitions teams. Despite institutional advantages in the purchasing process, such as the ability to pay in all cash or waive inspection contingencies, individual buyers have shown a willingness to outbid, and individual sellers tend to be very focused on headline numbers. This expected exuberance from individual buyers makes sense. Given the advantaged mortgage programs, tax subsidies, and cultural desire for homeownership, individuals should be willing to “overpay” for a home compared to an institutional buyer viewing it simply as a financial asset.

These factors add up to one conclusion: SFR is never coming back.

Or, to be more precise, the acquisition of individual properties to create single-family rental portfolios is done. Strategies that more closely mirror multifamily development, such as build-to-rent communities, are more likely to be feasible, depending on multifamily development dynamics. But BTR, even more so than SFR, pushes development further and further into open space suburbs, reducing some of the existing urban/suburban rent premium.

Nevertheless, the patterns that emerged during the 15-year SFR cycle that’s now drawing to a close can be used to identify and enable the next wave of institutional investment into a new class of residential real estate. While SFR might not be a viable institutional investment opportunity, institutions still have an appetite for real estate investment. And with major institutions openly discussing reducing allocation to office, and a bid-ask gap in traditional multifamily, there is demand to find another “next” asset class. Many of the technologies, processes, and strategies that accelerated the launch of SFR have the potential to be applied to similar asset classes. The question, then, is whether a class exists that is:

Not broadly institutionalized

Historically lower-performing/difficult to manage efficiently

Positioned for performance improvement using emerging tech/methods

Experiencing unique stresses as a result of the current economic crisis

Currently undervalued

For our answer, we turn to the cores of major US metro areas

Over the past few decades, major metro areas have experienced a massive increase in housing demand driven by job opportunities and improved urban amenities. At the same time, restrictive zoning policies have prevented the supply of housing from keeping up with this demand increase, leading to rapid, sustained housing price increases.

In 2020, this climb hit a wall. The early months of the pandemic drove millions of people out of cities. Residential landlords, used to perpetually climbing rents, found themselves having to deeply discount their units in order to maintain occupancy. Alongside government policy interventions that banned foreclosures for single-family homeowners, major cities put a moratorium on evictions with the goal of keeping people housed. Large property operators felt the stress but had tools available to those with scale to ameliorate the financial challenges: cash buffers, privileged banking relationships, and the ability to liquidate some assets to protect others. Smaller operators were subjected to the same stresses, with a far smaller toolbelt to navigate it. A building with three units, a non-paying tenant, no eviction rights, and no mortgage payment moratorium replicated many of the key elements of the financial distress wrought upon homeowners during the GFC. For the remainder of 2020, all of 2021, and early 2022, these conditions persisted, with many of the tighter regulations making small operations challenging long after the state of emergency was ended.

Demand for urban living began picking up again in 2022, resulting in rents reaching all-time highs in 20231. At the same time, the Federal Reserve’s decision to raise interest rates in response to inflation has made financing/refinancing real estate purchases, whether for owner-occupiers or for investment, significantly more expensive, putting downward pressure on residential real estate values even as rents continue to climb.

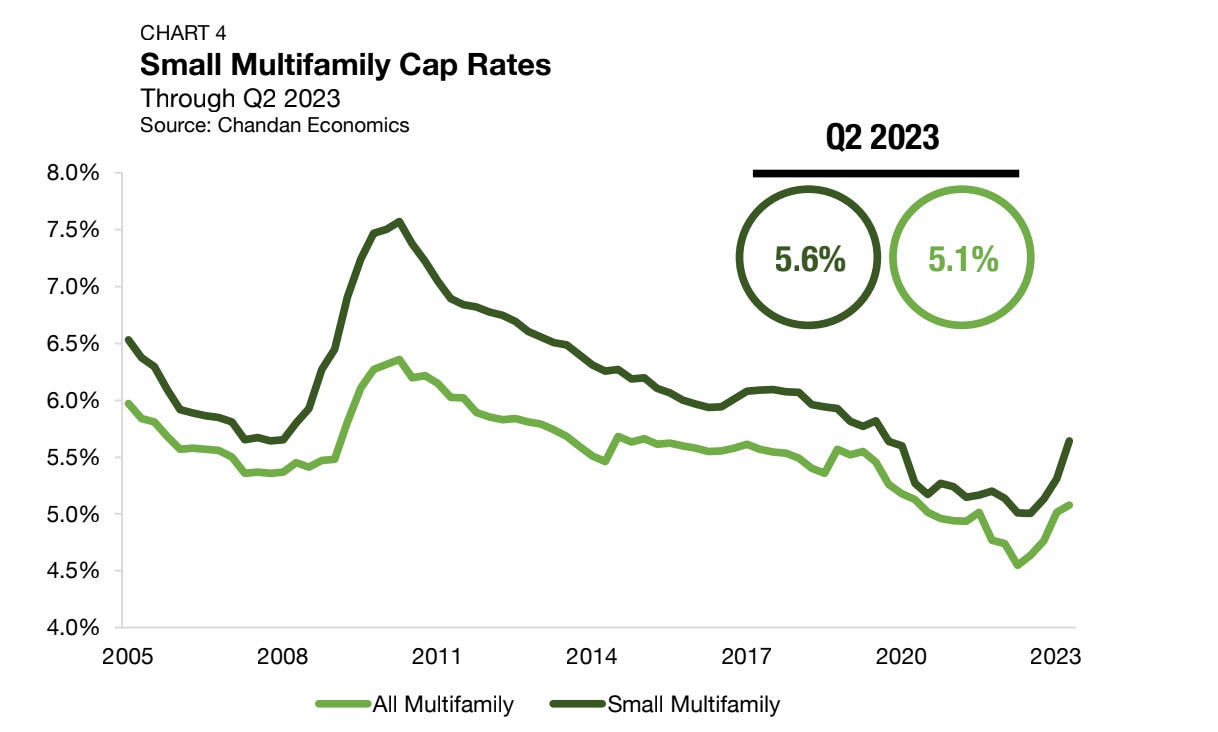

As shown in the graph above, sticker prices for multifamily real estate have dropped precipitously following rate hikes, while those of single-family homes have continued to climb, albeit more slowly than before the hikes. In large part, this is due to a different buyer pool. Millions of individuals are vying for single-family homes alongside institutional purchasers, whereas primarily institutions, operating under stricter financial return parameters, are active in the multifamily space.

Coupled with continuing rent increases, this increase in single-family home prices while multifamily asset prices decline is a very different pattern than was seen after the GFC. It suggests, amongst other things, that while SFR may not be a viable institutional model any longer, other multifamily residential real estate has room for significant value expansion if rates return to lower levels as is widely predicted in 2024 and 2025. This value gap is likely even greater for small multifamily, where cap rates tend to be higher than those of large multifamily and more reactive to rates and other pressures described above. Additionally, and perhaps in response to the pressures above, a large number of small multifamily operators, many of whom are individuals nearing retirement age, are looking to liquidate their assets or downscale their exposure to the stresses of day-to-day management, bringing additional supply onto the market.

Small buildings, big opportunity

Of the broadly undervalued multifamily residential class, which subset presents the best opportunity along other dimensions? Broadly speaking, one can divide residential assets into single-family (1 unit), small multifamily (2-50), and large multifamily (>50 units). Larger multifamily assets have traditionally been the core focus of institutional real estate, with single-family representing a recent institutional area of focus. With plenty of supply in SFR and only so much capital, the small multifamily sector has been largely absent from institutional focus. But our four remaining criteria–not broadly institutionalized, historically lower-performing, improvable with emerging tech/methods, and experiencing unique stresses–are largely satisfied by this class of real estate.

For example, in a Boston survey of over 17000 small multifamily rental properties, only 32% were owner-occupied (i.e. most are investment properties) and of the remaining 68%, 88% were owned by groups with three or fewer total properties. This lack of institutional focus and investment has generally relegated small multifamily to a bimodal fate: underinvestment from smaller operators who don’t invest the capital to bring them up to modern environmental and living standards, or condo developers who can turn a three-unit building into two or three higher-end condos with significant investment and a bet on the sale price outpacing the costs of acquisition and upgrade.

From a rental perspective, the size of the small multifamily asset class and the removal of the SFR asset class as a viable institutional investment opportunity presents a market for a next SFR-like asset class. There are over one million 2-20 unit buildings in the United States, which serves as a large base supply for a new asset class, what we call the Modern Urban Rental (MUR). MURs are upgraded experiences in non-amenitized 2-20-unit residential buildings in dense urban cores. Similar to SFR, operators typically upgrade interiors, utilities, and smart systems to improve resident experience, operational efficiency, and environmental sustainability while benefiting from increased rents and lower operating expenses than smaller, less-scaled operators.

MUR is the new SFR

MUR candidates are ubiquitous in cities across the US. They began to spring up en masse in the late 19th and early 20th centuries, driven by the combination of demand for cheap housing from waves of immigrants seeking opportunity in US cities and the absence of the zoning regimes that would soon spring up across the country and restrict further construction of MURs and other cost-effective housing typologies.

Historically, small multifamily properties have constituted the backbone of naturally occurring affordable housing in otherwise expensive cities. In the second half of the 20th century, broader urban trends in the US contributed to disinvestment in many of these properties even as investment flowed into newer large developments. Nevertheless, recent decades have seen an uptick in demand for all forms of urban housing, resulting in renewed interest in MURs from residents and investors alike.

Despite this, institutional ownership of MURs remains low given the operational challenges they present. Unlike SFRs, these are multi-unit assets, so far more maintenance tasks remain the responsibility of the property operator, not the single tenant user. Unlike large multifamily assets, MURs cannot rely on centralized, onsite staff who can respond quickly to maintenance requests and perform routine checkups without traveling from property to property. With traditional management practices, this results in significantly higher expense ratios, producing returns that are unattractive to institutional investors.

Fortunately, current MUR operators have the opportunity to build upon the SFR playbook, borrowing some elements of it while developing other practices from scratch. Many tech solutions that were successfully deployed in SFR, including smart locks and remote thermostat controls, are equally applicable to MUR. Similarly, data-driven bulk acquisition strategies are viable in both asset classes and necessary to speedily deploy capital with lower per-property analysis and soft costs. Lastly, bundling of service calls into geographic clusters and preventive maintenance can drive down operating costs, shaving critical percentage points off of expense ratios. In 2008, at-scale last-mile logistics players like Uber or Grubhub did not exist. Now they, and the logistics techniques they pioneered, are well-understood and replicable. Even Amazon only began experimenting with its own last-mile delivery solutions in 2009 and only scaled the program into its formal Amazon Logistics division in 2018. To this day, ~75% of deliveries for Amazon are still done by third parties like UPS, USPS, and FedEx.

MUR differs from SFR in key ways

Despite these similarities, the MUR asset class differs from SFRs in a number of ways, many of which align with current renter and societal preferences:

Sustainability/walkability: Nearly all MURs are located in dense, urban areas close to public transit options, as compared to SFRs, which are generally found in lower-density suburbs/exurbs. This results in lower carbon emissions and traffic congestion attributable to MURs. Additionally, MURs have lower average unit sizes and shared walls, meaning that the energy needed to heat and cool them is also substantially lower.

Preserving homeownership opportunities: Institutional ownership of SFRs has been criticized for taking homeownership opportunities away from individual buyers. While this narrative is often exaggerated–institutional investors only own 25% of SFRs, or 6% of all single-family homes in the US–it doesn’t hurt that, on the margin, institutional ownership of MURs preserves affordable rental opportunities without reducing the stock of homes available for individual ownership. This also reduces the likelihood of politicians threatening to punish the MUR industry via regulation.

Regulatory environment: A corollary to MURs being located primarily in older cities and SFRs being located primarily in newly developed suburban areas is that the predominant regulatory environments affecting the two classes differ greatly. Old cities like New York, San Francisco, and Boston are both highly restrictive in terms of their attitudes toward new development and present a wide variety of regulatory challenges for landlords. Newer suburban areas in the Sunbelt are the opposite, with favorable attitudes towards development and relatively straightforward policies regarding landlord/tenant relations. This contrast creates favorable conditions for large institutional landlords who operate MURs: the market value of their assets is buffered by the difficulty of adding new supply, and the complexity of tenant law gives them a competitive advantage relative to smaller operators who can’t invest in standardized compliance processes to the same degree.

More MUR, Less SFR

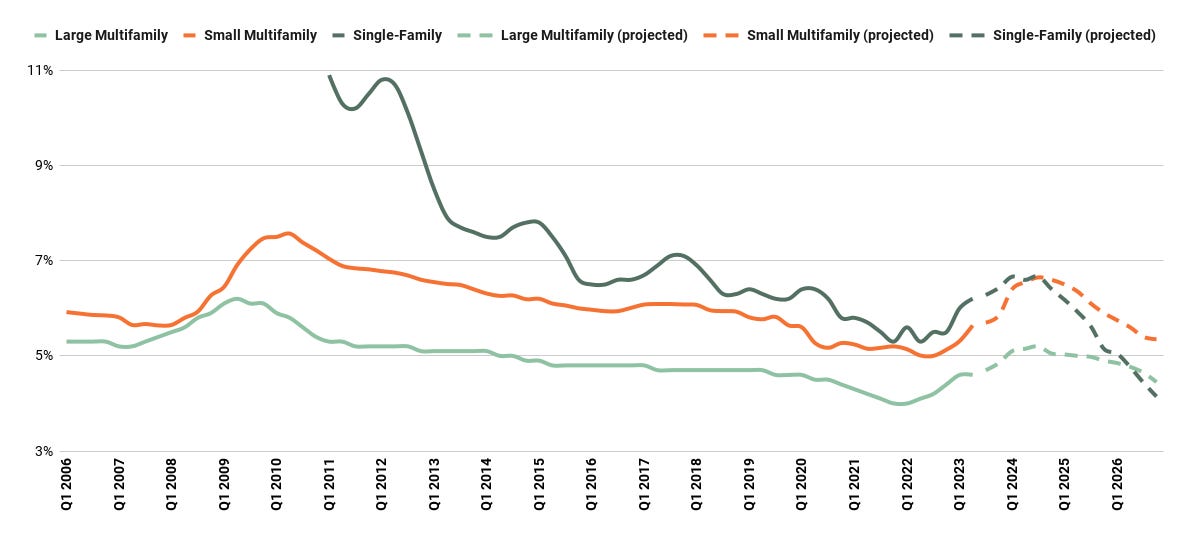

A widely cited report from MetLife predicts that institutions will own 40% of SFRs by 2030. There are two ways for that metric to be true. One option is that the SFR market will continue to grow, with institutions playing a larger role. MetLife projects that 7.6 million single-family homes will be SFRs by 2030. The second option, which we believe is more likely, is that the macro trends described above will cause the overall SFR market to shrink, with institutions owning a larger part of the smaller total. Based on the trends described in this report, we believe effective SFR cap rates will trend below those of small multifamily, and eventually below those of large multifamily, due to overwhelming demand and government subsidies for individual homeowners. This will price out institutional owners.

SFR, small multifamily (MUR) and multifamily cap rates. Historical data sourced from Arbor Realty and Chandan Economics, projections from Groma Research.

Excess institutional capital, searching for yield and in-demand residential assets, will be redirected to new asset classes, such as MURs, which are still recovering from the unique stresses that impacted them during the CFC. Current institutional ownership of the MUR asset class is de minimis and not widely tracked, similar to SFR in 2010. However, we predict that institutional ownership of this asset class will grow from current untracked levels to 20-25% by 2030, which would make MUR an institutional asset class consisting of hundreds of thousands of buildings and millions of units.

Many asset allocators are currently hesitant to deploy into real estate given uncertainty regarding interest rates, bond yields, and the broader macro environment. These concerns are legitimate–predicting the exact moment at which a given investment becomes the correct decision is inherently difficult. Nevertheless, we believe that as the market turns, that the small multifamily/MUR asset class is primed to be a key area of focus in this next cycle.

Notably, rents are not at an all-time high when adjusting for inflation. Nominal rents are used here given that property value data cited elsewhere in this essay is also nominal, enabling a consistent basis for comparison.